Comfortable and stress free retired life is what all of us want and when it comes to retirement financial insecurity is possibly the biggest stress hence a well thought out retirement plan is imperative for every individual. Key to build a well rounded retirement plan is to start early, stay disciplined and invest in assets which give inflation beating returns in long term. you can also talk to your financial advisor for a personalized retirement plan.

For years now PPF, EPF and saving instruments like fixed deposits and post office schemes have been the preferred destination for Indians to build their retirement corpus. But with ever decreasing PPF interest rate as well as decreasing rates on fixed deposits, going forward I believe they are not the best way to create a healthy retirement corpus.

Why PPF might not be as good as it is made to be

Interest rates on last 20 years have come down from high of 12 % to 8.1 % now. On the other hand Inflation in last 20 years has been hovering at a median of about 6.3 % , which means if PPF rates still go down your post inflation returns are going to be 1.5-2.0 % per annum only which might not be sufficient to build an healthy corpus.

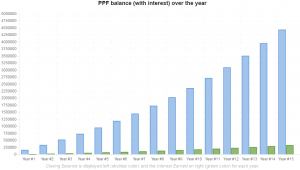

At the prevailing interest rates, if you invest 1.5 lacs which is the maximum amount you can invest in PPF, then at the end of 15 years, your maturity amount will be approximately 44.4 lacs. Out of 44.4 lacs, you would have earned an interest of approximately 21.8 lacs and your money you deposited was 22.5 lacs.

The other trend to note is Government has recently pegged PPF rates to inflation rates so interest rates can go down further. Govt has already reduced rates from 8.70 % last year to 8.1 % this year and I guess this will go down further.

Alternately, you can also invest this amount in a relatively safe equity mutual fund or in SIP. Let’s say we invest in large cap funds. They are relatively safe and can give returns in the range of 10-12 %.

Your total corpus at the end of 15 years will be approximately 63 lacs, which means approximately 50 % more than what your PPF account will give you.

What happens if Inflation is considered?

Now let’s study have a look at the effect of inflation. What inflation does is it increases the money you require to buy a basket of goods and hence reduces real returns on your investments and savings. Below graph tells you how inflation has trended in last few days

Now the median inflation has been around 6.3 % in last 20 years or so. Let’s assume inflation will be 6 % for next few years which means your effective PPF rate will be around 2.1 % and if you calculate inflation adjusted retirement corpus it will be approximately 27 lacs and you deposited about 22.5 lacs in your PPF account. In short inflation adjusted returns suck.

In case you invested in a portfolio of mutual funds your inflation adjusted return will be approximately 36.5 lacs much higher than PPF.

Advice from a Personal Finance Advisor

If you are investing a large part of your retirement corpus through PPF you need to rethink your strategy with reducing interest rates this is not the best option to plan your retirement savings.

If you are investing through fixed deposits it will be worst as fixed deposits attract TDS which reduces your returns further. It is time to start looking at equity markets to build sustainable retirement portfolio. For people who do not understand investments in stocks, investing in Mutual fund is a great way to start.

Veeramachineni Lalitha

I am Finance Content Writer. I write Personal Finance, banking, investment, and insurance related content for top clients including Kotak Mahindra Bank, Edelweiss, ICICI BANK and IDFC FIRST Bank. My experience details : Linkedin