Key Factors That Determine Your Home Insurance Premium

For many of us, our home is our most significant investment. Protecting it with homeowners’ insurance is essential, but the rising cost of premiums can leave us wondering if we are truly getting the best value for our money.

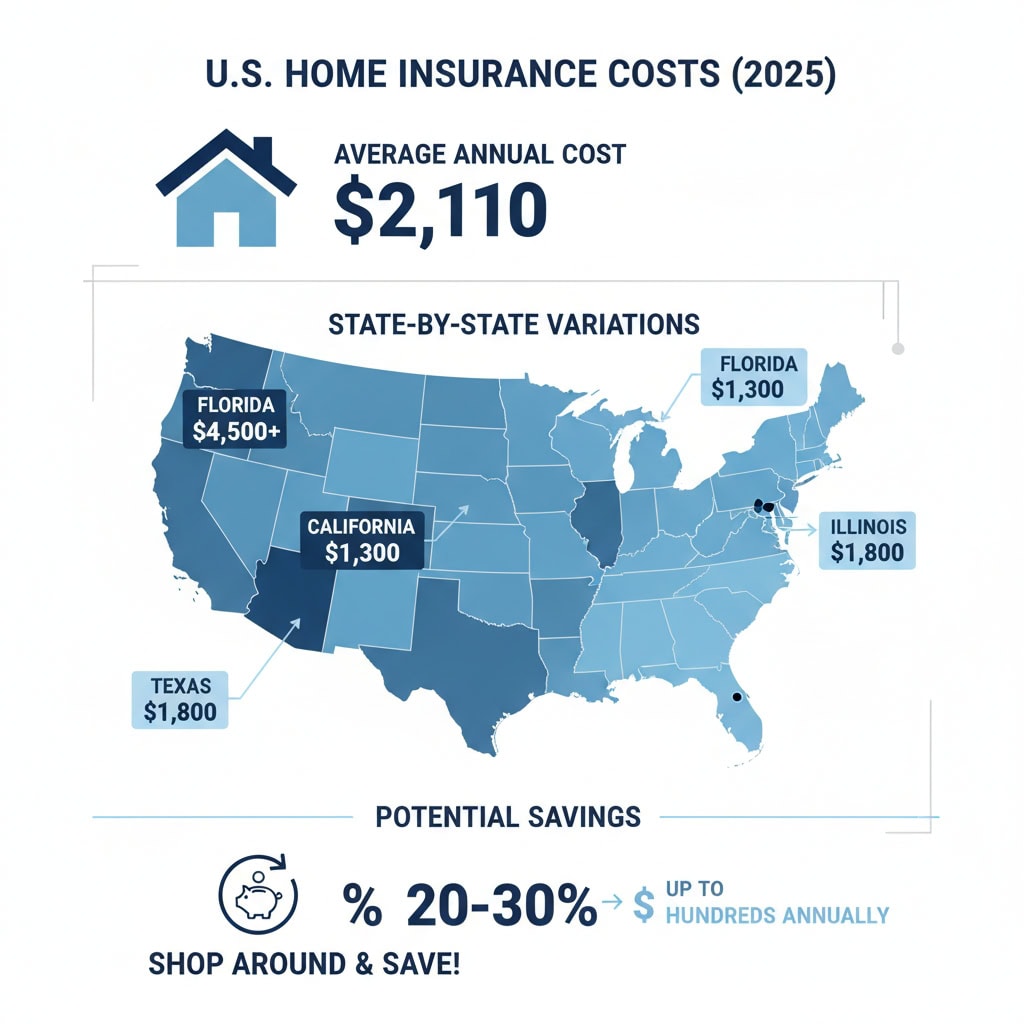

You are not alone if you feel this way. Across the country, homeowners’ insurance premiums are on the rise, with the average annual cost now around $2,110. Many homeowners believe they might be overpaying for their policies.

The good news is that we have the power to take control. Comparing home insurance premiums effectively can lead to significant savings and ensure we have the right coverage without overspending. In fact, active comparison shopping can save hundreds of dollars annually.

This comprehensive guide will walk you through everything you need to know. We will explore the key factors that influence your premium, show you how to compare quotes accurately, and reveal actionable strategies to lower your costs. Our goal is to empower you to make informed decisions for the protection of your home and your peace of mind. For a detailed guide on navigating this process, many homeowners find value in understanding Stanley’s home insurance comparison.

Understanding what drives your homeowners’ insurance premium is the first step toward effective comparison. Premiums aren’t arbitrary; they are carefully calculated based on a complex interplay of factors related to your property, its location, and your personal profile. By understanding these influences, we can better identify areas for potential savings and ensure we receive an accurate quote.

Your Home’s Characteristics

The physical attributes of your home significantly influence the cost of your insurance. Insurers assess the risk of damage or loss based on these details.

- Age of Home: Older homes often come with higher premiums. This is because their systems (plumbing, electrical, and heating) may be outdated, making them more prone to issues such as burst pipes or electrical fires. They might also feature materials that are more expensive or difficult to replace.

- Construction Type: The materials used to build your home directly impact its resilience to perils and the cost of repairs. For instance, a brick or concrete home might have a lower premium than a wood-frame house due to its superior fire resistance and durability.

- Roof Age and Material: Your roof is your home’s first line of defense against the elements. An older roof, or one made of less durable materials, is more susceptible to damage from wind, hail, and storms, leading to higher premiums. Conversely, a new roof or one made of impact-resistant materials can lead to discounts.

- Electrical and Plumbing Systems: As mentioned, outdated systems pose a higher risk. Modern, well-maintained electrical wiring and plumbing can reduce the likelihood of claims, thereby lowering your premium.

- Square Footage and Features: Larger homes generally cost more to insure because they require more materials and labor to repair or rebuild. Unique features, such as custom finishes, swimming pools, or elaborate landscaping, can also increase your premium due to higher replacement costs and potential liability.

Your Location and Risk Profile

Where your home is located has a profound impact on your insurance costs. Insurers analyze regional data to determine the likelihood of various risks.

- Risk of Natural Disasters: If your home is located in an area prone to specific natural disasters, such as hurricanes, tornadoes, wildfires, or earthquakes, your premium will reflect the increased risk. For instance, homeowners in coastal regions often face higher premiums and may need to purchase separate windstorm or flood insurance.

- Proximity to Fire Hydrants and Fire Departments: Homes closer to fire hydrants and professional fire departments generally have lower premiums. This is because emergency services can respond faster, potentially limiting damage in the event of a fire.

- Local Crime Statistics: High crime rates in your neighborhood, particularly for burglaries and vandalism, can lead to increased premiums. Insurers use localized data to assess this risk.

- Flood Zones: Standard homeowners’ insurance policies do not cover flood damage. If your home is located in a designated flood zone, you will need to purchase separate flood insurance, which will add to your overall protection costs. Understanding your specific location’s risk profile is crucial for accurate comparison.

Your Personal and Policy Details

Beyond your home and its location, your individual history and the choices you make about your coverage also influence your premium.

- Previous Claims History: A history of filing multiple claims, especially for preventable incidents, can signal higher risk to insurers and result in increased premiums.

- Credit-Based Insurance Score: In most states, insurers use a credit-based insurance score as a factor in determining premiums. A higher score often indicates a lower risk, which may result in better rates.

- Desired Coverage Amounts: The more coverage you opt for – whether for your dwelling, personal property, or liability – the higher your premium will be. It’s essential to strike a balance between adequate protection and affordability.

- Chosen Deductible: Your deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. A higher deductible typically results in a lower premium, as you assume more initial risk.

- Liability Limits: The amount of liability coverage you choose directly impacts your premium. Higher limits offer greater protection against lawsuits but come with a higher cost.

By understanding these intricate factors, we can approach the comparison process with greater clarity and identify opportunities to optimize our coverage and costs.

A Strategic Approach to Home Insurance Premium Comparison

Comparing homeowners insurance quotes effectively isn’t just about finding the lowest price; it’s about securing the best value – robust coverage at a competitive rate. This strategic approach involves careful preparation, understanding different purchasing avenues, and meticulous evaluation of offers.

Gathering Your Information for an Accurate Quote

To get accurate and comparable quotes, you’ll need to provide insurers with detailed information about your home and your personal history. Having this ready beforehand streamlines the process and prevents discrepancies between quotes.

Here’s a list of essential information you’ll need:

- Property Address: The exact location of your home.

- Year Built: The age of your home.

- Construction Details: Type of exterior (e.g., brick, vinyl siding), roof material (e.g., asphalt shingles, metal), and age of the roof.

- Home Dimensions: Square footage, number of stories, and number of bedrooms/bathrooms.

- Systems Information: Details about your heating, electrical, and plumbing systems, including their age and any recent upgrades.

- Security Features: Information on alarm systems, smoke detectors, fire extinguishers, deadbolts, and sprinkler systems.

- Unique Features: Presence of swimming pools, trampolines, wood-burning stoves, or other potential liabilities.

- Personal Information: Your name, date of birth, marital status, and social security number (for credit-based insurance score checks).

- Claims History: Details of any previous homeowners’ insurance claims you’ve filed in the last 3-5 years.

- Desired Coverage Start Date: When you need the policy to become active.

- Current Policy Details (if applicable): Your current coverage limits and deductible.

Having this comprehensive data ready will ensure that every insurer is quoting on the same basis, making your comparison truly “apples-to-apples.”

Choosing Your Path: Direct, Captive, or Independent Agent

When it comes to obtaining quotes, you generally have three main avenues, each with its own advantages:

- Direct-to-Consumer Carriers: These are companies that sell policies directly to consumers, often online or over the phone, without the use of an intermediary agent. This can be a quick way to get quotes if you’re comfortable navigating the options yourself.

- Captive Agents: These agents work exclusively for one insurance company. They are experts in their company’s products and can provide in-depth information about their specific policies and discounts. However, they can only offer you options from that single insurer.

- Independent Agents: An independent insurance agent works with multiple insurance companies. This allows them to shop around on your behalf, comparing policies from various providers to find the best fit for your needs and budget. The value of an established independent agent with decades of experience lies in their ability to provide personalized service, leverage their relationships with multiple carriers, and build long-term trust. They can often uncover options you might not find on your own. For a deeper understanding of working with agents, exploring resources such as property insurance companies can be beneficial. Additionally, for general consumer guidance and company information, state insurance departments, such as those listed by the NAIC, are excellent resources.

How to Compare Quotes Effectively

Once you’ve gathered your information and decided how you’ll get quotes, the real comparison begins. This step is crucial to ensure you’re not just focusing on the bottom line.

- Ensuring Identical Coverage Limits: The most crucial aspect of comparing quotes is to ensure that each quote provides the same coverage limits for dwelling, personal property, other structures, and liability. A lower premium might mean significantly less coverage.

- Matching Deductibles: Just as with coverage limits, ensure the deductible amounts are consistent across all quotes. A higher deductible will always result in a lower premium, but it means more out-of-pocket expense if you file a claim.

- Reviewing Endorsements: Endorsements (also called riders or add-ons) expand or modify your standard policy. If one quote includes coverage for water backup or identity theft protection, ensure other quotes offer similar endorsements for a fair comparison. For a comprehensive understanding of policy terms and endorsements, referring to a Glossary can be incredibly helpful.

- Looking Beyond Price: While cost is a major factor, consider the insurer’s reputation for customer service and claims handling. A slightly higher premium for a company with a stellar track record might be a worthwhile investment.

- Checking Insurer Financial Strength Ratings: Reputable rating agencies (like A.M. Best) assess an insurance company’s financial stability. A strong rating indicates the company has the financial capacity to pay out claims, even in widespread disaster scenarios.

- Utilizing Comparison Tools: Websites like HelpInsure.com can be valuable resources, allowing you to compare sample rates, complaint information, and financial ratings of various insurance groups. This can give you a broader perspective on the market. For a step-by-step walkthrough of the comparison process, many homeowners find value in understanding Stanley’s home insurance comparison.

By following these steps, we can move beyond superficial price comparisons to make a truly informed decision about our home insurance. For more detailed guidance on understanding your policy, exploring a comprehensive Home Insurance Policy guide can provide valuable insights.

Decoding Your Policy: Coverage, Costs, and Key Terms

Understanding the components of your homeowners’ insurance policy is fundamental to making an informed comparison. A policy isn’t just a single price; it’s a collection of coverages, each with its own limits and implications for your premium and potential payouts. Let’s break down the key terms and types of protection.

A standard homeowners insurance policy typically comprises several distinct coverage areas:

- Dwelling Coverage (Coverage A): This protects the physical structure of your home, including the foundation, walls, and roof. Its limit should be sufficient to rebuild your home entirely at current construction costs, not just its market value.

- Other Structures Coverage (Coverage B): This covers structures on your property not attached to your main home, such as detached garages, sheds, or fences. It’s typically a percentage (e.g., 10%) of your dwelling coverage.

- Personal Property Coverage (Coverage C): This protects your belongings inside and outside your home, including furniture, electronics, clothing, and appliances.

- Loss of Use Coverage (Coverage D) / Additional Living Expenses (ALE): If your home becomes uninhabitable due to a covered peril, this coverage helps pay for temporary living expenses, such as hotel stays, meals, and other necessary costs, while your home is being repaired.

- Personal Liability Coverage (Coverage E): This protects you financially if you or a household member is found responsible for bodily injury or property damage to others, whether it occurs on or off your property.

- Medical Payments Coverage (Coverage F): This covers medical expenses for guests injured on your property, regardless of fault, up to a specified limit.

For a deeper dive into what each section of your policy entails, exploring resources like Property Insurance Coverage can be very beneficial.

Replacement Cost (RCV) vs. Actual Cash Value (ACV)

One of the most critical distinctions in personal property coverage is between Replacement Cost Value (RCV) and Actual Cash Value (ACV). This choice has a significant impact on your premium and, more importantly, your payout in the event of a claim.

Feature Replacement Cost Value (RCV) Actual Cash Value (ACV)

Definition: Pays to replace damaged or stolen property with new items of the same kind and quality. Pays to replace damaged or stolen property minus depreciation (wear and tear, age).

How it’s Calculated: Based on the current market price of a new, equivalent item. An amount for depreciation is then subtracted from the current market price of a new item.

A premium impact generally results in a higher premium because the insurer pays out more in claims. Generally, it results in a lower premium because the insurer pays out less in a claim.

Payout Example (5-year-old TV originally $1,000, new equivalent $1,200, 50% depreciated). You receive $1,200 (the cost of buying a new, similar TV). You receive $600 ($1,200 new cost – $600 depreciation). Choosing RCV provides more comprehensive protection, ensuring you can replace your belongings without incurring significant out-of-pocket expenses due to depreciation.

The Role of Deductibles

As discussed earlier, the deductible is the amount you pay out-of-pocket before your insurance company begins to pay for a covered loss. Understanding its role is crucial for managing your premium.

- Definition of a Deductible: It’s your financial contribution to a claim. For example, if you have a $1,000 deductible and incur $5,000 in covered damages, you pay the first $1,000, and your insurer pays the remaining $4,000.

- Impact on Premium: There’s an inverse relationship between your deductible and your premium. Choosing a higher deductible typically lowers your annual premium, as you’re assuming more of the initial risk. Statistics show that raising your deductible from $1,000 to $2,500 can lower your rate by an average of 11%.

- Dollar Amount vs. Percentage-Based Deductibles: Most standard deductibles are a fixed dollar amount ($500, $1,000, $2,500). However, some policies, especially in high-risk areas, may have percentage-based deductibles for specific perils (e.g., 1% or 2% of your dwelling coverage for hurricane or wind damage). This means your deductible could be much higher for those specific events.

- Choosing a Deductible You Can Afford: While a higher deductible saves you money on premiums, select an amount you can comfortably afford to pay out of pocket if you need to file a claim. An unaffordable deductible defeats the purpose of having insurance. For more insights on managing this aspect, refer to our guide on Help with Insurance Deductible.

Understanding Peril Policies for a Smart Home Insurance Premium Comparison

Homeowners insurance policies are generally categorized by how they define covered perils (the causes of loss). This distinction significantly impacts what’s covered and, consequently, your premium. For a deeper understanding of the various policy types, our guide, “What Are the Different Types of Home Insurance,” offers valuable insights.

- Named Peril Policies (HO-2): These policies are more restrictive. They only cover damage caused by perils specifically listed (or “named”) in the policy. Common named perils include fire, lightning, windstorm, hail, explosion, riot, aircraft, vehicles, smoke, vandalism, theft, falling objects, weight of ice/snow/sleet, and accidental discharge or overflow of water or steam. If a peril isn’t on the list, it’s not covered.

- Open Peril Policies (HO-3, HO-5): These policies offer broader protection. They cover damage from all perils except those specifically excluded in the policy. HO-3 (special form) is the most common type, covering the dwelling for open perils and personal property for named perils. HO-5 (comprehensive form) is the most extensive, covering both the dwelling and personal property for open perils.

- Common Exclusions: Even open peril policies have exclusions. The most common ones include floods, earthquakes, war, nuclear hazards, and sometimes mold or sewer backups (though these can often be added as endorsements).

- How Policy Type Affects Cost: Named peril policies (such as HO-2) generally have lower premiums because they offer narrower coverage, thus presenting less risk to the insurer. Open peril policies (HO-3, HO-5) come with higher premiums due to their comprehensive protection. When comparing, ensure you understand which type of policy you’re being quoted for and if it adequately addresses your risk tolerance.

By carefully analyzing these policy elements, we can make a truly informed comparison of home insurance premiums, ensuring our coverage aligns with our needs and expectations.

Actionable Strategies for Lowering Your Insurance Costs

Finding the right home insurance premium isn’t just about comparing quotes; it’s also about proactively implementing strategies to reduce your risk profile and qualify for discounts. Many homeowners feel they are overpaying for their policy (59% of Zebra customers, for example), but with a few smart moves, we can often significantly lower our annual costs.

Opening Common Home Insurance Discounts

Insurance companies offer a variety of discounts to policyholders who demonstrate lower risk or loyalty. Don’t leave money on the table – always ask your insurer about these potential savings. For a comprehensive look at how to reduce your expenses, consult our guide on Ways to Save Money on Homeowners Insurance.

- Protective Devices Discount: Installing safety and security features can lead to significant savings. This includes burglar alarms, smoke detectors, carbon monoxide detectors, sprinkler systems, and even smart home technology that monitors for leaks or fires.

- New Home Credit: If you’ve recently purchased a newly constructed home, you may qualify for a discount due to the use of modern building codes and materials.

- Claims-Free Discount: Many insurers reward policyholders who haven’t filed a claim for a certain period (e.g., 3-5 years) with a discount. This highlights the benefit of avoiding small claims.

- Mature Homeowner Discount: Policyholders over a certain age (often 55 or 65) may be eligible for discounts, as they are frequently perceived as more responsible and less likely to file claims.

- Home Improvements: Upgrading key home systems can reduce risk and earn discounts. This includes replacing an old roof, updating electrical wiring, or upgrading plumbing.

- Impact-Resistant Roof Discount: In areas prone to hail or windstorms, installing an impact-resistant roof can significantly lower your premium.

- Gated Community/HOA Discount: Living in a community with improved security or fire protection services provided by an HOA might qualify you for a discount.

The Power of Bundling: Combining Home, Auto, and More

One of the most effective ways to save on insurance is to bundle multiple policies with the same provider.

- How Bundling Saves Money: Insurers often offer significant discounts when you purchase more than one type of policy from them. This is because they value your loyalty and the increased business.

- Combining Home and Auto Insurance: This is the most common and often most lucrative bundling option. The average saving can be substantial; for instance, bundling home and auto insurance can save you an average of 5% on auto insurance alone, plus additional savings on your home policy. For more details on this strategy, refer to our article on Bundle Home and Auto Insurance.

- Potential for Bundling Life or Business Insurance: Depending on the insurer, you might also be able to bundle other types of coverage, such as life insurance, umbrella liability, or even small business insurance, for additional savings.

- Convenience of a Single Point of Contact: Beyond savings, bundling offers the convenience of managing all your insurance needs through one company, simplifying payments and claims.

Proactive Steps for a Better Home Insurance Premium Comparison

Beyond discounts and bundling, several ongoing practices can help you maintain lower insurance costs and ensure you’re always getting the best deal.

- Improving Your Credit Score: As noted, your credit-based insurance score can impact your premium. Maintaining a good credit history can lead to better rates in most states.

- Performing Regular Home Maintenance: Keeping your home in good repair, addressing small issues before they become large problems (like leaky pipes or damaged roofs), reduces the likelihood of filing claims.

- Avoiding Small Claims: While insurance is designed for major losses, consider paying out of pocket for minor repairs that are only slightly above your deductible. Filing numerous small claims can increase your future premiums or even lead to non-renewal.

- Reviewing Your Policy and Shopping Around Annually: Insurance rates and your needs can change. It’s wise to review your policy at least once a year, or whenever you have a significant life event (like a major renovation, new valuables, or a change in family status). This is also the ideal time to shop around and compare quotes from different providers. Even if you’re satisfied with your current insurer, obtaining competitive quotes can give you the leverage to negotiate a better rate. Our guide on Insurance Rate Inflation underscores the importance of this regular review.

- Considering Increased Coverage: When Should We Consider Increasing Our Homeowners Insurance Coverage? If you’ve made significant renovations, purchased expensive new belongings, or your local construction costs have risen, your current dwelling and personal property limits might be insufficient. It’s crucial to ensure that your coverage keeps pace with the value of your home and your belongings.

- Understanding Underinsurance: What are the potential consequences of underinsuring our home or belongings? If your coverage limits are too low, you could face substantial out-of-pocket expenses to rebuild your home or replace your possessions after a major loss. This can lead to severe financial strain and negate the purpose of having insurance.

By actively engaging in these strategies, we can empower ourselves to not only save money on home insurance but also ensure we have the comprehensive protection our most valuable asset deserves.

Veeramachineni Lalitha

I am Finance Content Writer. I write Personal Finance, banking, investment, and insurance related content for top clients including Kotak Mahindra Bank, Edelweiss, ICICI BANK and IDFC FIRST Bank. My experience details : Linkedin