Key Takeaways:

- Recent federal policy changes are capping federal student loan amounts, leading more students to consider private loans.

- Private student loans often come with higher interest rates and fewer borrower protections compared to federal loans.

- It’s crucial for students to explore all financing options, including scholarships and grants, before resorting to private loans.

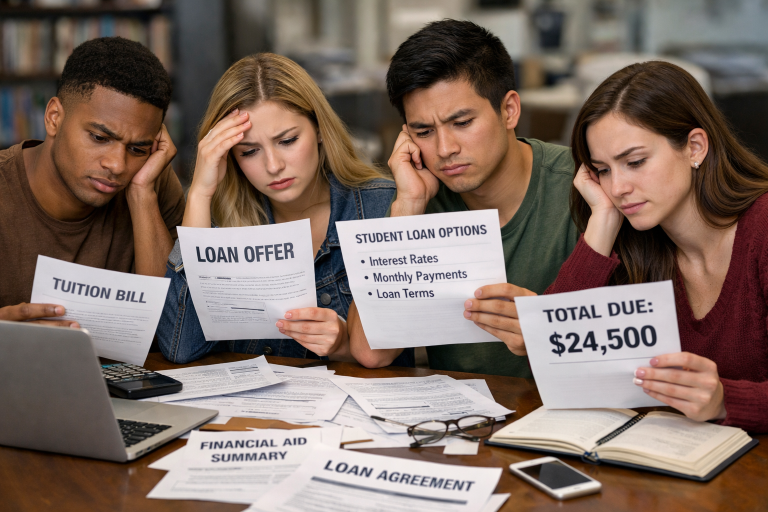

With the cost of higher education climbing and federal student loan caps on the horizon, families and prospective students are navigating an increasingly complex financing landscape. Private loans are filling a growing gap for college-bound students, yet this shift brings its own risks and considerations. Understanding how options like the best private student loans fit into the broader context of paying for college is crucial.

Federal student loans have traditionally served as the backbone of college funding in the United States, but looming changes to borrowing limits mean that more families must explore private alternatives. As students face new challenges when securing funds for their education, it becomes even more critical to stay informed about the implications of this evolving financing model.

Federal Loan Caps and Their Impact

Beginning July 1, 2026, new federal rules will cap student loan borrowing. Graduate students will be limited to borrowing a lifetime maximum of $100,000, while parents taking out loans on behalf of their children will face a lower cap of $65,000. These federal loan caps are designed to limit excessive borrowing and reduce the risk of over-indebtedness, but they also push more students toward the private loan market. These changes could leave thousands of families looking elsewhere for additional funding, fundamentally shifting who can afford a graduate or professional education.

The Rise of Private Student Loans

As federal support shrinks, private student loans are becoming a primary, if not necessary, bridge for educational costs. Unlike their federal counterparts, private student loans often have higher interest rates and less forgiving repayment terms, which can increase the total cost of borrowing and make repayment more challenging. As detailed in a recent CNBC report, these loans generally lack flexible repayment plans or forgiveness options, raising concerns about the long-term financial burdens graduates may face.

This growing reliance on private student loans requires new borrowers to pay closer attention to loan terms and the fine print. Many lenders require either a good credit score or a co-signer, which can be another hurdle for students fresh out of high school or college. The trend is part of why understanding every aspect of a loan agreement before signing is essential, as repayment hardships can significantly affect financial health well beyond graduation.

Challenges in Qualifying for Private Loans

Items such as credit scores and the presence of a willing co-signer often become make-or-break qualifiers for private loan applicants. According to a study highlighted by WTOP News, about 40 percent of private loan applicants are denied due to either insufficient credit history or inability to secure a qualified co-signer. For many students, this reality can disrupt educational plans or lead to reliance on riskier financial products, such as high-interest personal loans or credit cards, both of which carry additional financial risks.

Exploring Alternative Financing Options

Before turning to private lenders, students and their families should look for opportunities that do not require repayment. Scholarships and grants are the most advantageous sources of funding and are available from schools, private organizations, and government agencies. Applying broadly and early is key. Federal and institutional work-study programs also provide a means for students to earn money while attending classes, reducing reliance on loans. Additionally, a growing number of employers now offer tuition reimbursement and educational assistance as employment benefits, which can significantly offset out-of-pocket costs for working students.

Taking time to research eligibility requirements, deadlines, and application strategies can improve the chances of securing funding. Many students overlook smaller or niche scholarships, which often have less competition and can add up significantly. Combining multiple funding sources allows for a more flexible and sustainable financial plan throughout one’s academic journey.

- Scholarships and Grants: These are awarded based on merit, need, or specific talents and do not need to be paid back.

- Work-Study Programs: Part-time jobs, often campus-based, help students cover daily living and educational expenses.

- Employer Tuition Assistance: Some workplaces now offer education benefits, allowing employees to continue their education with financial support from their employer.

Understanding the Risks of Private Loans

Variable interest rates, strict credit requirements, and the absence of income-based repayment or forgiveness programs are a few of the major risks associated with private student loans. Variable rates can cause monthly payments to fluctuate, adding uncertainty to borrowers’ financial planning. Without federal protections such as hardship deferment or public service loan forgiveness, those with private student loans may struggle to find flexibility if their financial circumstances change. These realities underscore why it’s so important for families to research all alternatives and, if possible, consult with a financial advisor before making long-term commitments.

Conclusion

The evolving landscape of college financing demands careful planning and thorough research. With private student loans taking on a bigger role in funding higher education, families must study every avenue before borrowing. Knowing the limits of federal aid, the gaps private loans can fill, and the risks they carry can make the difference between educational dreams realized and unsustainable debt. Exploring all available resources, such as scholarships, grants, work-study, and employer support, gives students the best chance at affording their education without compromising their future financial well-being. Tools and advice available through large publications and government resources can further guide borrowers toward sound decisions that support long-term success.

Veeramachineni Lalitha

I am Finance Content Writer. I write Personal Finance, banking, investment, and insurance related content for top clients including Kotak Mahindra Bank, Edelweiss, ICICI BANK and IDFC FIRST Bank. My experience details : Linkedin