Understanding Bad Credit Loans and Modern Financial Services

In May 2026, the landscape of personal finance has evolved significantly, particularly for individuals navigating the challenges of a less-than-perfect credit history. Traditional lending institutions often rely heavily on FICO scores and extensive credit histories to assess risk. A FICO score of 670 or higher is typically preferred by most conventional lenders. However, this narrow focus can exclude many otherwise responsible borrowers who have experienced past financial setbacks or simply haven’t had the opportunity to build a robust credit profile.

Defining the Bad Credit Landscape

“Bad credit” generally refers to a FICO score below 670, with scores under 580 often considered “poor.” This classification can be the result of various factors, including late payments, high credit utilization, defaults, or even a lack of credit history altogether. Borrowers in this category often face higher interest rates and stricter terms from traditional lenders, if they are approved at all. The key challenge for these individuals is finding financial solutions that acknowledge their current financial stability and future earning potential, rather than solely focusing on past credit missteps.

The Role of Specialized Financial Services

This is where Tio Rico financial services and non-traditional lenders step in. Many modern lending platforms recognize that a credit score doesn’t tell the whole story. Companies like Upstart, for instance, are known for approving borrowers with credit scores as low as 300, and even those with no credit history. They leverage AI-driven underwriting models that consider a broader range of factors, such as education, employment, and income, offering a more holistic view of a borrower’s financial health. Similarly, OppLoans and Avant focus on overall creditworthiness, often utilizing “soft credit checks” that do not negatively impact an applicant’s FICO score. This approach allows them to provide access to funds for individuals who might otherwise be denied by conventional banks.

The market in May 2026 continues to see innovation in this space, with a growing emphasis on financial inclusion. Lenders like Oportun cater specifically to those with limited or no credit history, approving loans for amounts as small as $300. These entities are crucial in providing essential financial lifelines, ensuring that temporary financial difficulties or a lack of credit history don’t completely shut individuals out of necessary borrowing opportunities.

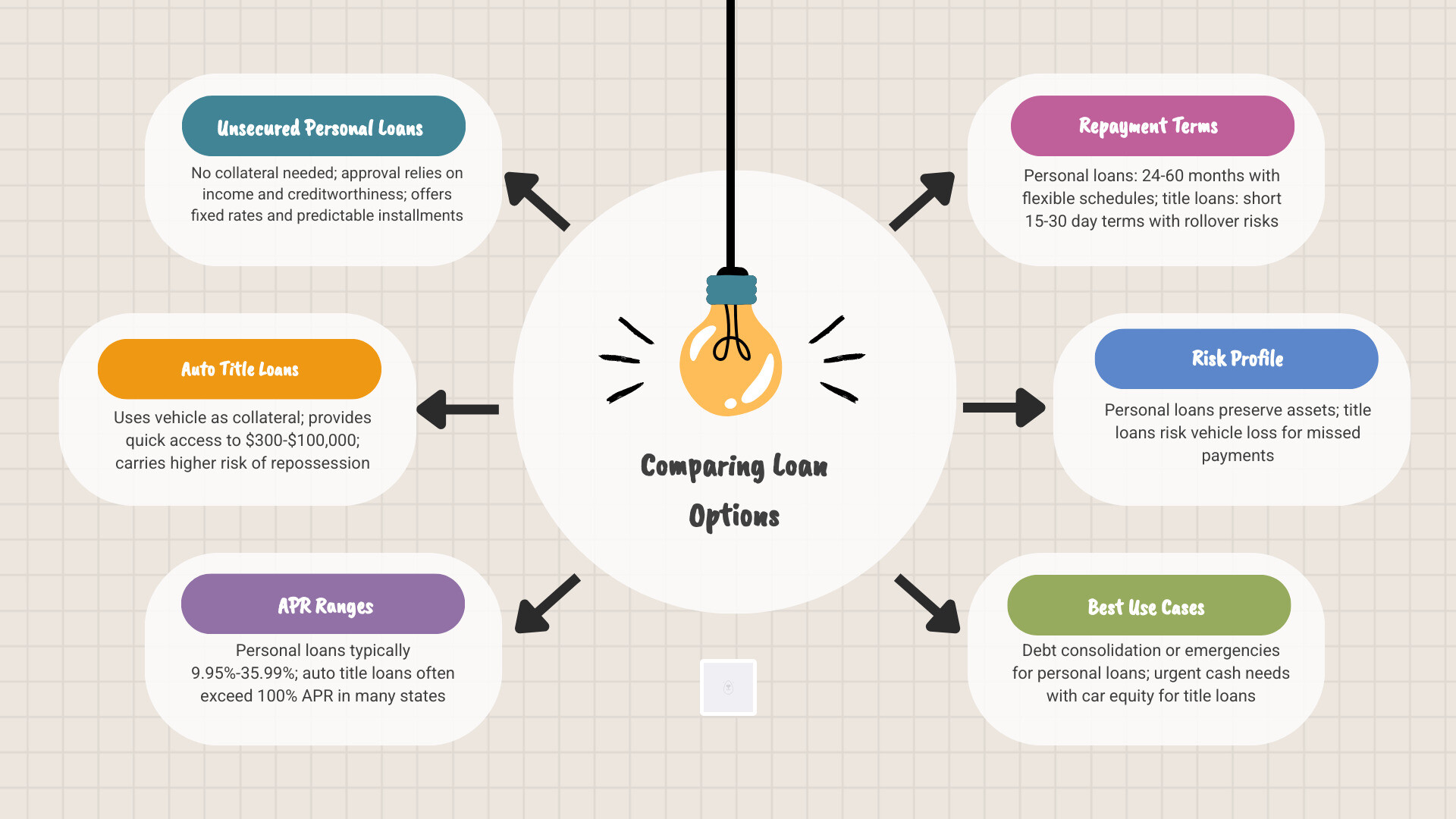

Comparing Personal Loans and Auto Title Loan Structures

When exploring loan options with bad credit, two common types that often emerge are personal loans and auto title loans. While both can provide much-needed funds, their structures, requirements, and inherent risks differ significantly. Understanding these distinctions is crucial for making an informed decision.

Unsecured Personal Loan Features

Unsecured personal loans are a form of unsecured financing, meaning they do not require collateral. Lenders assess your eligibility primarily based on your income, employment stability, and overall creditworthiness, rather than your FICO score alone. These loans typically come with fixed rates and predictable monthly installments, making budgeting easier. Loan amounts can vary widely, from a few hundred dollars to tens of thousands. For example, Avant offers personal loans ranging from $2,000 to $35,000 with terms between 24 and 60 months, and APRs from 9.95% to 35.99%. California Bank & Trust offers unsecured loans from $2,500 up to $100,000, with APRs typically ranging from 12.19% to 28.16%. Many unsecured personal loans also boast benefits like no prepayment penalties and potential rate discounts for automatic payments. These loans are often used for debt consolidation, major expenses, or emergency costs, providing repayment flexibility without putting personal assets at risk.

Auto Title Loan Mechanics

Auto title loans, on the other hand, are a type of collateralized debt. These loans use your vehicle’s clear title as collateral, meaning the lender holds the title until the loan is repaid. This makes them accessible even for individuals with very poor credit or no credit history, as the primary qualification factor is the equity in your vehicle. Loan amounts are determined by the vehicle’s value, and can range from small sums like $200 up to $1,500, or even more, depending on the lender and state regulations. For instance, some providers offer personal loans that function similarly to title loans, requiring vehicle registration in your name but not necessarily full ownership, meaning you can still be making payments on your car.

While auto title loans can offer quick access to funds, they often come with higher APRs compared to many personal loans, though typically lower than predatory payday loans which can reach APRs as high as 400%. Some providers, like Cash Time in Arizona, offer personal loans from $200-$1,500 without requiring a vehicle inspection, simply needing the vehicle to be registered in your name. Funds are often disbursed quickly, sometimes on the spot via check. If you default on an auto title loan, the lender has the right to repossess your vehicle, which is a significant risk.

Eligibility and the Application Process for Financial Services

Securing a loan, especially with a less-than-ideal credit history, hinges on understanding the specific eligibility requirements and navigating the application process efficiently. While traditional lenders often prioritize high credit scores, specialized financial services focus on a broader range of indicators to assess your ability to repay.

Eligibility Requirements for Specialized Financial Services

For many non-traditional lenders, age requirements (typically 18 years or older) and proof of a stable income are fundamental. Lenders need assurance that you have the financial capacity to make regular payments. This often involves providing recent pay stubs, bank statements, or other documentation to verify your employment and income. Residency verification is also standard.

A crucial factor for all lenders is your debt-to-income (DTI) ratio, which indicates how much of your gross monthly income goes towards debt payments. A lower DTI ratio signals to lenders that you have more disposable income available to cover new loan payments.

For personal loans that cater to bad credit, some lenders have minimum credit score requirements, such as Universal Credit’s minimum of 560. However, many, including Upstart and Oportun, are more flexible, accepting applicants with no credit history or very low scores. These platforms often consider factors like educational background, employment history, and income stability.

For auto title loans, the primary eligibility requirement is owning a vehicle with a clear title (or at least having it registered in your name, even if you’re still making payments). The vehicle’s value determines the potential loan amount. Some lenders may perform a quick vehicle valuation but might not require a physical inspection. It’s also important to note that active military personnel and their dependents are typically prohibited from obtaining certain types of loans due to the Military Lending Act.

Steps to Secure Funding

The application process for specialized financial services is often streamlined for speed and convenience. Here’s a general overview:

- Prequalification (Optional but Recommended): Many lenders offer a prequalification process that involves a “soft credit check.” This allows you to see potential loan offers and estimated rates without impacting your credit score. Companies like Axos Bank, OppLoans, Experian, and LendingTree all emphasize this no-impact prequalification step. This is an excellent way to shop around and compare options.

- Gather Your Documents: Before formally applying, have your documents ready. This typically includes a government-issued ID, proof of income (pay stubs, tax returns), proof of residency (utility bill), and bank account information. For auto title loans, you’ll also need your vehicle’s title and registration.

- Complete the Application: Applications can usually be completed online, over the phone, or in person. Online applications are often the quickest, with some lenders offering decisions in minutes.

- Verification and Approval: Once submitted, the lender will review your information. For personal loans, this might involve verifying your income and employment. For auto title loans, it will include a vehicle valuation. Many specialized lenders aim for same-day approval, with funds potentially disbursed as soon as the same business day if approved early enough (e.g., OppLoans if approved by 12 PM CT). Other lenders, like Avant, might provide funding as early as the next business day, while Axos Bank aims for funds within two days of the final loan agreement.

- Receive Funds: Approved funds can be deposited directly into your bank account via ACH transfer, or in some cases, you might receive a check or cash in person.

By understanding these eligibility requirements and following the application steps, you can significantly improve your chances of securing the necessary funding, even with bad credit.

Managing Risks and Identifying Predatory Lending Practices

While loans for individuals with bad credit can be vital financial tools, they often come with higher risks, primarily due to elevated interest rates and fees. It is paramount to approach these options with caution and a keen eye for identifying predatory lending practices.

Alternatives to Traditional Financial Services

Before committing to a high-interest bad credit loan, it’s wise to explore alternatives. Credit unions are often a more borrower-friendly option; as not-for-profit organizations, they may offer more flexible lending criteria and lower interest rates than for-profit lenders. Many federal credit unions offer Payday Alternative Loans (PALs), which are small loans with APRs capped at 28% and loan amounts up to $2,000, significantly more affordable than traditional payday loans.

Other alternatives include:

- Borrowing from friends or family: This can be a low-cost option, but it’s crucial to have clear terms and a repayment plan to avoid straining relationships.

- Paycheck advance apps: Services like these can provide small advances on your paycheck, but be aware that associated fees can translate to effective APRs near 36%.

- Secured credit cards or credit-builder loans: These are designed to help improve your credit score over time by demonstrating responsible repayment.

- Community organizations and hardship programs: Many local and national non-profits offer financial assistance or low-interest loans for specific needs.

- Budgeting loans: In some regions, government-backed budgeting loans are available for individuals on certain benefits, offering interest-free options for essential expenses.

Improving Future Approval Odds

Taking steps to improve your creditworthiness can open doors to better loan terms in the future.

- Reduce your Debt-to-Income (DTI) ratio: Lenders look at your DTI to assess your ability to take on new debt. Paying down existing debts or increasing your income can lower this ratio.

- Make on-time payments: Payment history is a major component of your credit score. Consistently paying all your bills on time is the single most effective way to improve your credit.

- Consider a co-signer: If a trusted individual with good credit is willing to co-sign your loan, it can significantly improve your approval odds and potentially secure a lower interest rate. However, the co-signer is equally responsible for the debt.

- Secured credit cards: These cards require a cash deposit as collateral, making them easier to obtain with bad credit. Using them responsibly can help build a positive credit history.

- Dispute credit report errors: Regularly check your credit reports from all three major bureaus (Experian, TransUnion, Equifax) via AnnualCreditReport.com. If you find any inaccuracies, dispute them immediately, as errors can unfairly lower your score.

Identifying Predatory Lending Practices

Unfortunately, the need for quick cash can make individuals with bad credit vulnerable to predatory lenders. These lenders exploit desperate situations with unfair terms, high fees, and misleading practices.

Red flags to watch out for:

- Triple-digit interest rates: Payday loans are notorious for APRs that can soar as high as 400%. Car title loans, while sometimes lower, are still significantly higher than other bad credit loans. We strongly advise against loans with APRs exceeding 36%, as this threshold is often considered the maximum for affordable credit.

- Guaranteed approval: Reputable lenders always assess risk. Any lender promising “guaranteed approval” regardless of your credit is likely a scam.

- Upfront fees: Legitimate lenders typically deduct origination fees from the loan proceeds, not demand payment before funds are disbursed.

- Pressure to act immediately: Predatory lenders often create a sense of urgency to prevent you from carefully reviewing terms or seeking alternatives.

- Lack of transparency: Be wary of lenders who are vague about fees, interest rates, or repayment terms. Always demand a clear, written loan agreement.

- No credit check claims: While some specialized lenders use soft checks, be extremely cautious of those advertising “no credit check” loans, as these often come with exorbitant costs designed to trap you in a debt cycle.

To protect yourself, always verify a lender’s licensing and registration with your state’s Attorney General or relevant financial regulatory body. If you encounter a scam or suspect predatory practices, report it to the FTC Internet Crime Complaint Center (IC3). Your proactive steps can not only protect you but also prevent others from falling victim.

Frequently Asked Questions about Bad Credit Financing

Navigating loans with bad credit can bring up many questions. Here, we address some of the most common inquiries to help clarify your options in May 2026.

What is the typical interest rate for a bad credit loan in 2026?

The interest rates for bad credit loans can vary significantly based on the lender, the type of loan, your credit profile, and the overall economic climate in May 2026. For personal loans from specialized lenders, APRs typically range from around 9.95% to 35.99%, as seen with Avant. However, some platforms like OppLoans, which partner with banks to offer loans to those with lower credit, may have APRs ranging from 160% to 195%. It’s crucial to be aware that predatory loans like payday loans can have APRs as high as 400%. We generally advise borrowers to avoid any loan with an APR exceeding 36%, as this is often considered a benchmark for affordable credit. Always compare offers and choose the lowest APR you qualify for.

How does an auto title loan impact my credit score?

The direct impact of an auto title loan on your credit score depends on the lender’s reporting practices. Many auto title lenders do not report your payment history (positive or negative) to the major credit bureaus. This means that while taking out the loan might not directly harm your score, making on-time payments won’t necessarily help build your credit either. However, some lenders, like Cash Time in Arizona, state that they report to major credit bureaus when you make payments, which can help improve your credit score. If you default on an auto title loan and your vehicle is repossessed, this event itself is generally not reported to credit bureaus, but the underlying debt might eventually be sold to a collections agency, which would negatively impact your score. It’s essential to ask the lender about their credit reporting policies before you commit.

Can I get a loan if I have no credit history at all?

Yes, absolutely. In May 2026, several lenders and financial services are designed to cater to individuals with no credit history, often referred to as having a “thin file.” Companies like Upstart and Oportun are notable examples. Upstart approves borrowers with no credit history by using AI to evaluate factors beyond traditional credit scores, such as education, employment, and income. Oportun also specializes in approving loans for individuals with no credit history, often for amounts as low as $300. These lenders understand that a lack of credit history does not equate to a lack of creditworthiness. They offer a valuable entry point for building a credit profile, as many of them will report your on-time payments to credit bureaus, helping you establish a positive credit history for future financial endeavors.

Conclusion

Navigating loans with bad credit in May 2026 requires a blend of financial literacy, careful research, and responsible borrowing practices. While traditional lending avenues may seem closed, a growing ecosystem of specialized financial services offers viable solutions tailored to your unique circumstances.

We’ve explored the nuances of bad credit loans, distinguishing them from their traditional counterparts and highlighting the innovative approaches taken by modern lenders. We’ve also delved into the specifics of personal loans and auto title loans, outlining their features, eligibility requirements, and application processes. Crucially, we’ve emphasized the importance of identifying and avoiding predatory lending, which can trap borrowers in cycles of debt.

The key takeaway is empowerment. By understanding your options, comparing terms, and prioritizing your long-term financial health, you can make informed decisions. Whether you choose a personal loan with fixed monthly installments or an auto title loan for immediate needs, always ensure the repayment schedule—be it bi-weekly, semi-monthly, or monthly—fits comfortably within your budget. Responsible borrowing today is your pathway to improved financial stability tomorrow.

Veeramachineni Lalitha

I am Finance Content Writer. I write Personal Finance, banking, investment, and insurance related content for top clients including Kotak Mahindra Bank, Edelweiss, ICICI BANK and IDFC FIRST Bank. My experience details : Linkedin